What happens if you die without a will?

19th November 2015

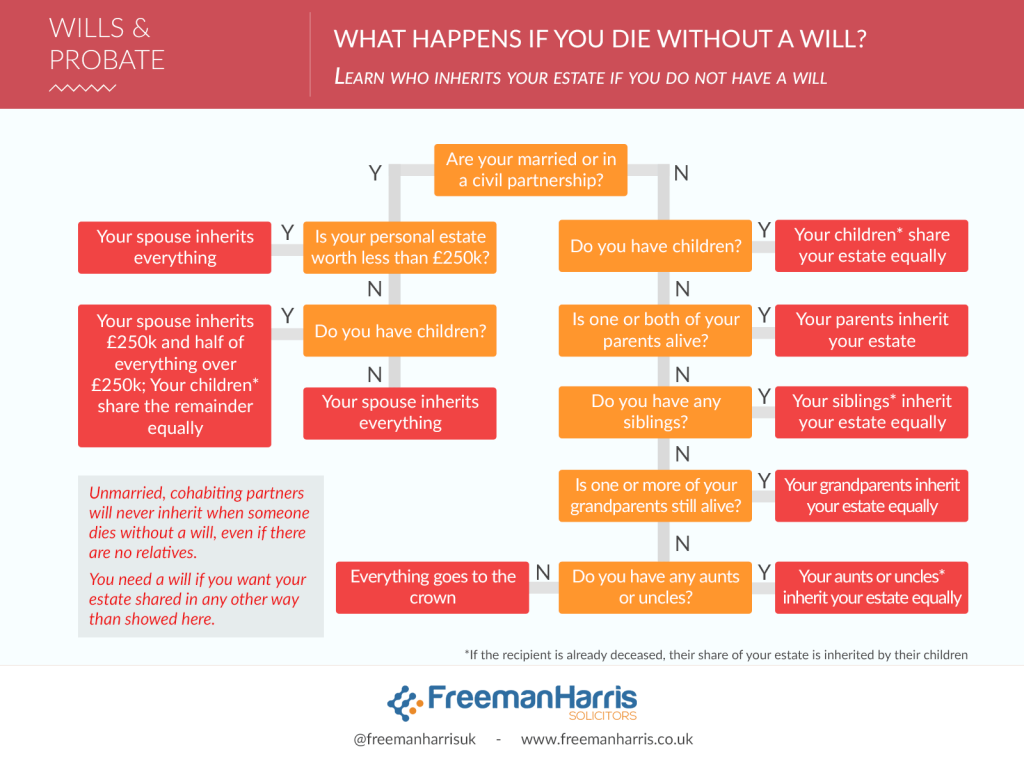

When someone dies without a will it is called dying “intestate.” When this happens, the deceased’s assets are shared out…

You may receive property from another person during their lifetime or on their death through their will. Whichever way you come into this gift, there are a number of tax implications for both the giver and the receiver to consider.Receiving a gift of property from a person during their lifetime.

Most people give away their assets during their lifetime in an attempt to minimise their IHT bill on death. By giving property away in this way effectively carves out the value of the property from the person’s estate thereby deflating it.

Read frequently asked questions about Wills

Capital Gains Tax – The donor will not pay CGT when they dispose of their home if it is their main residence and they have lived in the property for all the time it was owned. This is a tax relief known as Private Residence Relief. If the donor is disposing of property that is not their main residence however such as a business premises or buy-to-let, then it will be treated differently for CGT as follows.

CGT is calculated on the difference of value between the original purchase price and the date of disposal i.e. when the donor makes the gift. CGT is calculated on the gain and taxed at the donor’s income tax rate. The donor can also utilise their personal CGT allowance for that tax year to minimise the bill and deduct any allowable expenses as well.

Inheritance Tax – The donor has to survive for 7 years post giving the gift to be totally exempt from paying any IHT and anything short of that term, specifically between years 4 – 7 can mean a tapered IHT bill.

If you are a beneficiary and receive a property under the terms of a person’s will, the gift has similar tax consequences for both the testator and beneficiary.

Capital Gains Tax – none

Inheritance Tax – Your estate will include the net value of all your assets and the excess above the IHT threshold of £325,000 will be subject to 40% tax. Of course this can be mitigated by ensuring that gifts are made to ‘tax exempt’ people such as certain family members or to a charity when the rate of IHT is lower. The introduction of the Residence Nil Rate Band means that leaving your main home to lineal descendants will increase your tax free threshold by a further £175,000 (current tax year 2020/2021) so that the value of your main home of up to a maximum of £500,000 can pass through your will tax free.

Save for this, the only way to ensure that your IHT bill is low or non-existent is simply to reduce the value of your estate before death and that would mean giving your assets away during your life- time. In the event however that tax is due, this would need to be paid from your estate at the time of applying for probate which would be the responsibility of your Executors.

There are many problems besides tax that may arise when gifting your home. These are just some of the things you should consider:

Many clients wish to gift their home in order to prevent the local authority from forcibly selling their property in order to pay for care home fees. If you are going or plan to go into residential care, then the local authority will check whether there has been a deliberate deprivation of assets. The local authority can carry out a financial assessment to determine the amount of funding you are entitled to and it takes into consideration not only your currently owned property but also previously owned assets as well. This means that any gifted property can also be included in their calculations.

If you would like more information on how Freeman Harris can assist you or your family with making a will or probate and estate administration, please contact our team on 020 7790 7311 or email us at contact@freemanharris.co.uk.

Are you about to inherit or gift a property?

If so, discuss your matter with us first to know your rights and obligations.